Estate Planning involves setting up a plan that establishes who will eventually receive your assets. It also makes known how you want your affairs to be handled in the event you are unable to handle them on your own for any reason. It’s a complicated process, and it can definitely feel overwhelming. There are many components to Estate Planning, and while there’s a common misconception that it’s just about your finances, the truth is there’s a lot more to it.

There’s no denying that Estate Planning seems like a daunting chore, but it’s something we all need to face. We’ve broken the process down into easy-to-understand sections. Following our Estate Planning 101 guide will give you the security that comes with knowing you’ve planned for the future of your loved ones.

What is Estate Planning?

Estate Planning is simply the process of making it clearly known how you want your estate to be handled after you pass or if you’re incapacitated and unable to handle things on your own. The most common Estate Planning definition is — "the process of making plans for the management and transfer of your estate after your death, using a Will, Trust, insurance policies and/or other devices." Estate Planning has been around for many years, but it’s becoming increasingly more and more common.

There are many parts of Estate Planning, but the first thing you must do is conduct a comprehensive review of your estate assets. Your estate is made up of all the property you own, including:

Cash

Cars

Clothes

Jewelry

Houses

Investments

Savings

Retirement accounts

Land

And more

After you have a clear idea of what your estate is made up of, you can then begin planning.

Basics of Estate Planning

Estate Planning is important for many reasons. Perhaps the biggest benefit is if you don’t properly prepare for what should happen in the future while you’re sound and capable, you’ll have no say in how your estate is handled or what your loved ones receive when that time comes. Planning today ensures your tomorrow is exactly as you envision it.

A properly prepared Estate Plan will lay out your wishes exactly, in the most tax-advantage manner, so you can trust there won’t be any questions, misunderstandings or misconceptions about what you want.

Most Common Estate Planning Documents

Several documents will make up your Estate Plan. Each is important in its own way, and together they form a powerful representation of your final wishes.

Guardianship

States what you want to have happen and who you want to care for your children or any other dependent you’re responsible for after your death or in the event you’re no longer able to care for them. Most often, instructions for guardianship will be included in a section of your Will.

Will

A legal document that expresses your last wishes for distribution of your property or other assets.

Trust

A legal three-party fiduciary agreement that allows the first party (the Settlor, also may be referenced as Trustor or Grantor) to give the second party (the Trustee) rights to hold assets and property on behalf of and for the benefit of the third party (the Beneficiary).

Financial Power of Attorney (POA)

A legal document that gives someone the power to handle your financial affairs.

Durable Power of Attorney (POA)

A variation of a Financial Power of Attorney, which is a document that gives legal rights to another person so they can handle any of your non-health or non-medical affairs. “Durable” simply means that even if you become incapacitated, the POA remains in effect.

Advance Healthcare Directive (AHCD)

Also sometimes referred to as a Living Will or a Medical Power of Attorney. An Advance Healthcare Directive directly states what, if any, medical actions should be taken if you become incapacitated and unable to make your own decisions.

Note: it’s important to understand that while the terms “Living Will,” “Medical Power of Attorney” and “AHCD” are commonly used interchangeably, there are legal distinctions between them.

A Living Will lets you specify your medical preferences (typically for end of life decisions, like life support).

A Medical Power of Attorney lets you designate someone else to make healthcare decisions for you if you are unable to do so.

An AHCD combines the Living Will and Medical Power of Attorney to let you give instructions but also designate someone else to make decisions for you if needed.

HIPAA Authorization

Consent you give that allows your medical records or information to be shared with a third party.

Estate Planning & Taxes

Much of your Estate Planning is done with taxes in mind. The ultimate goal is to leave the absolute most you can to your heirs. Strategizing by taking action to minimize assets lost to taxes is an effective way to achieve your goal. There are some tools you can use within your Estate Plan, including ways to avoid probate and pass assets while avoiding hefty taxes. Understanding potential types of taxes is important.

Estate tax: A tax imposed on estates worth more than a set value. The tax is only assessed on the amount that exceeds the maximum, not the entire value of the estate.

Inheritance tax: A tax paid by someone who inherits either property or money from someone who has died.

Gift tax: A tax that’s applied on gifts exceeding a certain dollar amount. Note the giver, not the receiver, is responsible for any tax.

Who Needs an Estate Plan?

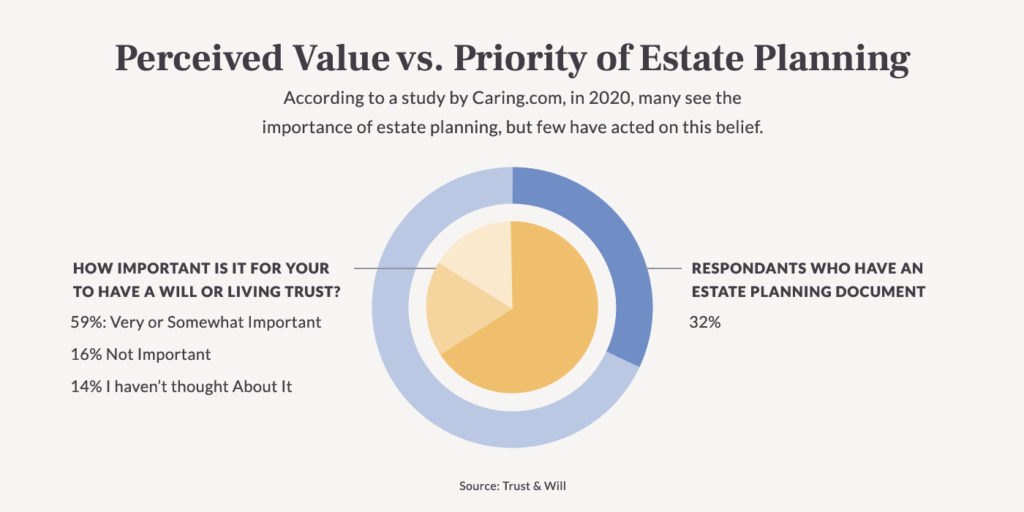

Short answer: Everyone. It’s easy to try and convince ourselves that we don’t need an Estate Plan. But the reality is, we would all be better off if we were planning a little more for our future. You don’t need to be wealthy, or elderly or even have a specific amount in your bank account to justify the need for a valid Estate Plan. If you are over the age of 18, you should start thinking about creating a plan.

Even if you don’t have a lot of assets, your Estate Plan is a guarantee that everyone will know what your wishes are. Health directives and long-term healthcare wishes are perfect examples of this – if you were ever to become incapacitated and couldn’t make your wishes known, your Estate Plan will speak for you, so your loved ones don’t have to make unthinkable decisions or wonder what you would want.

It used to be that properly preparing the types of documents that go in an Estate Plan could cost you thousands. But now you have options. You can get an affordable, legal, effective, valid Estate Plan that ensures your wishes will be known should the time ever come it’s needed. Even if you don’t have a lot of assets, an Estate Plan is still a wise idea.

How to Create an Estate Plan in 12 Steps

Yes, there are a lot of steps that go into creating a complete Estate Plan, but we’ve made it as easy as possible for you by listing each out.

Gather your assets. Inventory everything you own, from cars to collectibles.

Protect your family. Think about if you have adequate life insurance to leave your family in a position where they could maintain the life you currently lead.

Determine the plan that’s best for you. Decide what type of Estate Plan you need.

Choose who you would like to be guardian of your children/pets/self. If you have children or pets, or if you care for another loved one who cannot care for themselves, you want to choose a guardian. You can also name the person you would want to make medical and/or financial decisions on your behalf should you ever become unable to do so for yourself.

Determine and establish the necessary directives. There are several directives you should include in your Estate Plan, including but not limited to:

Durable Power of Attorney

Medical care directive

Limited Power of Attorney – LPOAs are less commonly used (Durable POAs are more frequently the norm), though an LPOA can be appropriate in some instances.

Name your Beneficiaries. Some documents and accounts will have Beneficiaries already designated. These could include retirement plans and life insurance policies, to name a few. But there are other assets you should note in your Will or Trust if you’d like to leave them to a specific person. If there is an opportunity, you should name contingent Beneficiaries. Keep in mind that Beneficiary designations will only go into effect after you pass, so if you become incapacitated and unable to make decisions, you need to have prepared for more than simply naming Beneficiaries.

Find a trusted partner. Explore your options for creating your Estate Plan. This can be face-to-face with an attorney or you may choose to use another service provider. You have options, but some are going to be much more expensive than others. If you don’t have an overly-complicated estate, working with a partner like Trust & Will could be the perfect solution to starting on the path of Estate Planning.

Create your plan. If you’re using an online program to create your Estate Plan, be sure to go through all the steps and finalize everything.

Sign and notarize your Estate Plan. Don’t forget to check how many witnesses your state requires.

Notify your Executor. It’s a good idea to let the person you chose to be your Executor know of your intentions.

Store your Estate Planning documents. Put your Estate Plan in a safe place where your loved ones can easily find it. A fireproof safe is a good idea.

Update as needed over time. There isn’t a hard rule about when you should update your Estate Plan, but a good rule of thumb is try to update it whenever you have a major life event (birth of a child, death of someone important to your plan, marriage, divorce, etc.). And if you find you haven’t had any life events in recent years, try to review and update as needed every 3 - 5 years.

Common Estate Planning Mistakes to Avoid

Take caution when developing your Estate Plan. There are many mistakes that could result in delays, inaccuracies or other misunderstandings. Some of the common mistakes people make along the way include:

Not having an official plan

Not updating a plan over time (at major lifetime events)

Not making arrangements for if they become incapacitated (disability or long-term care)

Improper ownership of assets (how easy will it be to pass assets on)

Not including charitable gifts

Not appointing a guardian for children or others who would need their care

Underestimating the implication of taxes

Not having liquidity of assets

Not making gifts during their lifetime to reduce the value of the estate after passing (tax advantages)

Putting their child’s name on the deed to property (potentially huge tax implications)

Difference between an Estate Plan and a Will

While many people think simply having a Will is sufficient, the fact is you need more. If you have a Will, you’re off to a great start. But a Will by itself is just a small piece of the Estate Planning puzzle. In order to fully protect your loved ones after you pass, you must incorporate all the documents, nominations and appointments to ensure you’ve done everything you can to make the process easier on them when the time comes.

Other Common Questions about Estate Planning

What Are Beneficiary Designations?

A Beneficiary designation is a way to designate where your assets go after you pass.

What Does a Trustee Do?

A Trustee handles and is responsible for managing all assets or property in a Trust. In essence, he or she is the legal owner of said assets.

How Much Does an Estate Plan Cost?

The cost of creating an Estate Plan can widely vary, depending on a number of factors. If you go the traditional route and work face-to-face with an attorney, your cost will be much higher. Newer methods of Estate Planning include innovative and creative platforms like Trust & Will, where you can get a legal Estate Plan at a fraction of the cost.

Do I Need an Attorney to Create an Estate Plan?

In some cases, you do not need an attorney to create your Estate Plan. If you have a very complicated estate, you may opt to go the traditional face-to-face route. But many people have simple, straight-forward needs. They may find a service like Trust & Will is ideal for their Estate Planning needs. It can save time and money while still offering a superior product that touches on all the important things you want to take care of with your Estate Plan.

Though there are many parts to a complete Estate Plan, tackling them one at a time is the best way to draft a plan that’s conclusive, comprehensive, thorough and that protects everyone in your life you love.

Share this article