Are Today’s Consumers “Financially Literate”?

Only 27% of Americans have a financial advisor. Explore what’s driving low engagement—and how the industry can better reach underserved groups.

By Maya Powers

Estate Planning Content Expert, Trust & Will

The role of financial advisors in estate planning is only relevant if clients engage with them in the first place. Our study found that 27% of respondents currently have a financial advisor, while 73% do not. While this figure might seem unsurprising, it underscores a critical gap in financial advisory engagement—particularly among younger generations, lower-income households, and certain demographics.

Generational Demands

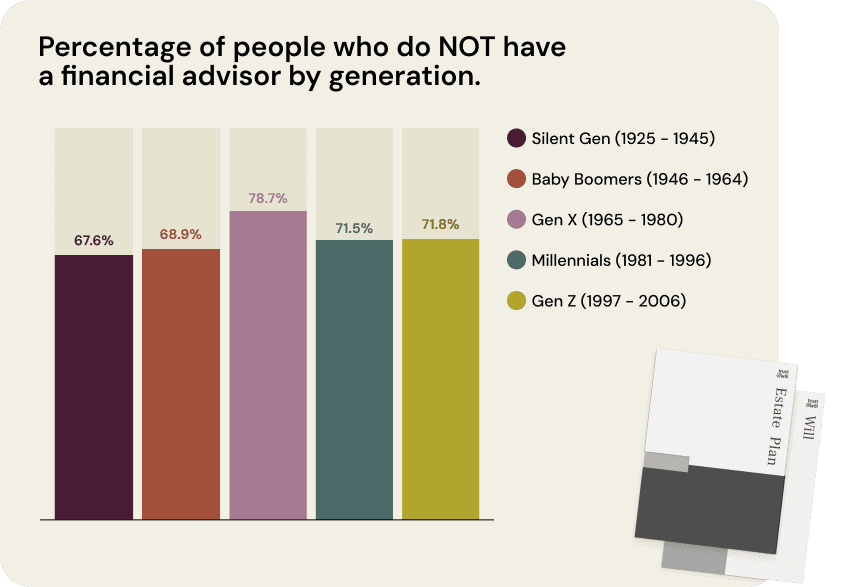

Contrary to common assumptions, financial advisor usage is relatively stable across generations. While older generations are often perceived as more likely to seek professional financial guidance, our study found that the Silent Generation (32%) and Baby Boomers (31%) are only slightly more likely to work with an advisor than Millennials (29%) and Gen Z (28%). In fact, Gen X had the lowest engagement rate (21%), which may indicate a segment of mid-career professionals who are navigating financial decisions independently rather than seeking expert guidance.

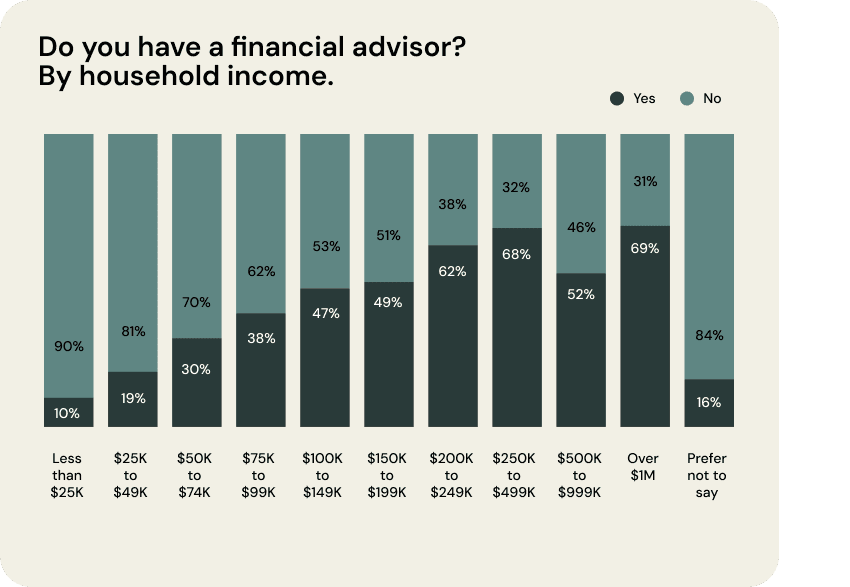

Household income strongly correlates with financial advisor usage, as expected. The higher the income, the more likely someone is to have an advisor. Only 10% of those earning under $25,000 reported working with an advisor, while 69% of those earning over $1M do. However, an interesting trend emerges in the mid-to-upper income brackets: financial advisor engagement dips among those earning between $500K-$999K (52%), before rising again among those earning over $1M. This suggests a threshold at which some affluent individuals either rely on personal financial management or seek alternative financial planning solutions.

Geographic & Political Trends

Regional differences in financial advisor engagement were not significant, but Northeastern residents were the most likely to work with an advisor (29%), while those in the Southeast were the least likely (25%). Suburban residents (30%) were also more likely to engage with an advisor than urban (27%) and rural (22%) residents.

When it comes to political affiliation, Libertarians (39%) and Green Party members (46%) were the most likely to work with financial advisors, outpacing both Democrats (27%) and Republicans (32%). While financial planning is often perceived as a neutral industry, this data suggests that certain political ideologies may align with a greater emphasis on structured financial planning and investment strategies.

Gender, Education & Racial Differences

A gender gap exists in financial advisor engagement: men (32%) are more likely than women (24%) to have a financial advisor. This disparity may be influenced by historical financial norms, confidence levels in financial decision-making, or differences in financial priorities.

Education also plays a significant role. Those with a higher level of education are more likely to work with an advisor, reinforcing the idea that financial literacy and exposure to wealth management concepts drive engagement. In contrast, only 9% of those with less than a high school education reported working with a financial advisor, compared to 51% of those with a doctorate degree or higher.

Racially, Asians (32%) were the most likely group to work with a financial advisor, followed by White (28%), Native (27%), Biracial (26%), Black (24%), and Hispanic (23%) respondents. This highlights a potential accessibility gap, as Black and Hispanic respondents tend to have lower financial advisor engagement rates despite often expressing a high level of interest in financial planning services.

The Key Takeaway for Advisors

For financial advisors, this data presents a clear opportunity to expand their reach—particularly among younger generations, middle-income earners, women, and minority groups. Many individuals, especially in underrepresented demographics, recognize the value of financial planning but may not know how to engage with an advisor or feel that these services are inaccessible to them.

At the same time, the broad generational stability in advisor engagement suggests that the industry may need to rethink how it connects with consumers. If younger generations are just as likely as older ones to work with advisors, but overall engagement remains low, what’s stopping the remaining 73% from seeking financial advice?

Expanding financial literacy, increasing awareness of affordable planning options, and emphasizing estate planning as a key component of a holistic financial strategy could help bridge this gap—ensuring that financial advisors aren’t just serving the wealthiest clients, but providing guidance to a broader, more diverse population.

These insights were unveiled in the Trust & Will 2025 Annual Financial Advisor Report. Click here to view the full report.

Trust & Will is an online service providing legal forms and information. We are not a law firm and we do not provide legal advice.

Last updated: March 20, 2026

- Share