The Financial Future and the Cost of Living Crisis

Trust & Will's 2025 Estate Planning Report reveals how Americans are feeling about the financial future and the growing financial divide.

By Maya Powers

Estate Planning Content Expert, Trust & Will

As economic uncertainty and rising costs reshape financial planning, Americans are increasingly concerned about their ability to build wealth, secure their future, and leave behind a meaningful legacy. Inflation, financial instability, and shifting economic opportunities are influencing not just daily financial decisions but also long-term estate planning and wealth transfer.

Nearly half (49%) of Americans say they are more concerned about their financial future now than they were last year, underscoring a growing anxiety about personal financial security. Inflation has made it somewhat or much harder for nearly four in five Americans (78%) to achieve their life goals. These concerns—combined with the pressures of rising costs, wealth inequality, and changing workforce dynamics—paint a complex picture of financial planning in the modern era.

Financial Anxiety and End-of-Life Concerns

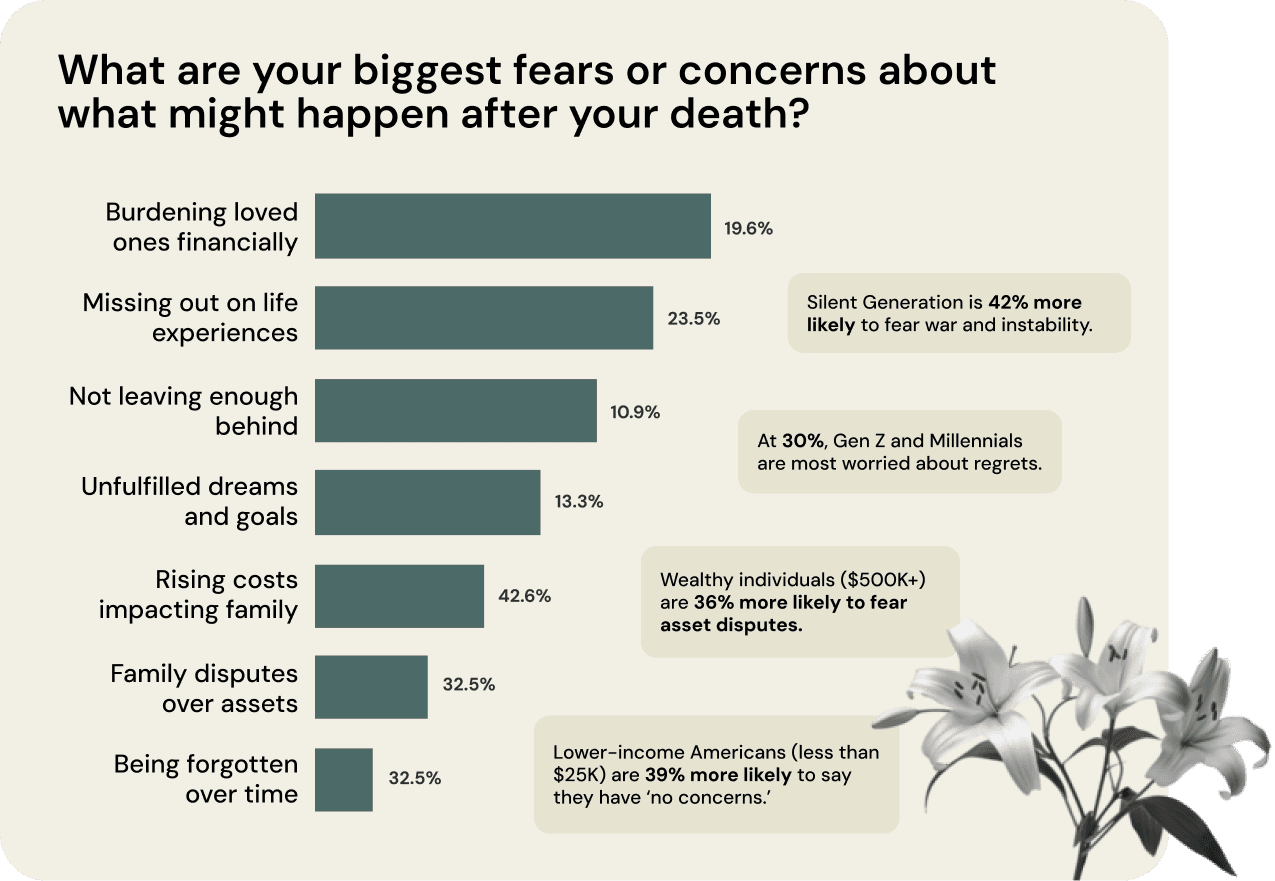

Financial worries don’t stop with life—they extend into how Americans think about their death. When asked about their biggest fears regarding what happens after they die, financial burdens were among the top concerns, but they were far from the only ones:

32% fear burdening their loved ones with financial or legal responsibilities.

30% worry about missing out on life experiences and moments with family and friends.

29% fear not leaving enough behind for their loved ones.

23% regret unfulfilled dreams and goals.

19% worry that rising costs—like healthcare and housing—will make it harder for their family to afford the future.

14% fear family disputes over their assets.

12% fear their legacy will be forgotten over time.

These concerns differ significantly by generation and financial status. Younger Americans are far more likely to express existential fears about regrets and missing out on experiences, while older generations focus more on financial and geopolitical stability:

Gen Z (30%) and Millennials (27%) are the most worried about unfulfilled dreams and goals.

The Silent Generation is 42% more likely than average to fear the impact of war, violence, or instability on their family's safety.

Lower-income individuals (earning <$25K) are 39% more likely than average to say they have “no concerns” at all.

Wealthier individuals ($500K–$999K) are 36% more likely than average to worry about family disputes over their assets.

These findings suggest that financial security does not eliminate posthumous concerns—it reshapes them. While lower-income respondents may have fewer estate planning worries, wealthier individuals are more focused on legal complexities, inheritance disputes, and securing their family’s future.

Americans’ Financial Outlook: Hope or Uncertainty?

Despite these concerns, many Americans maintain a cautiously optimistic outlook about their financial future. When asked how they feel about their personal finances and long-term opportunities:

33% say they are “cautiously optimistic”—hopeful, but aware of challenges.

23% say they are “optimistic,” feeling confident about meeting financial goals.

19% are “neutral,” neither optimistic nor pessimistic.

14% say they are “pessimistic,” believing personal or systemic challenges will make financial success difficult.

13% are “uncertain,” unsure about what the future holds.

However, financial optimism is highly dependent on income, education, and demographics:

56% of those earning over $1M feel optimistic, compared to only 14% of those earning under $25K.

The lower the education level, the higher the uncertainty: 31% of those with less than a high school diploma are uncertain about their financial future, compared to just 5% of those with a doctorate.

Men (27%) are more optimistic than women (20%), while women (15%) are more uncertain than men (9%).

Non-white respondents (26%) are more likely to be optimistic than white respondents (20%), though white respondents are more likely to be pessimistic (15%).

These findings suggest that optimism is often tied to financial security, but education and cultural perspectives also play a key role.

The Growing Divide in Financial Concern

When comparing financial outlooks year-over-year, one of the most shocking insights emerges: 49% of Americans are more concerned about their financial future than they were last year, 32% say their level of concern has stayed the same, and only 19% say they are less concerned.

At first glance, financial worry follows a predictable trend—the less you earn, the more anxious you are. However, this pattern breaks down dramatically at higher income levels:

Among lower-income groups (earning <$25K), 53% say they are more concerned than last year.

Concern steadily declines with income—only 32% of those earning $250K–$499K are more concerned.

But at $500K–$999K, financial concern jumps drastically to 71%—a staggering 122% increase from the previous bracket.

Even among those earning over $1M, 47% say they are more financially anxious than last year.

This unexpected reversal suggests that financial concern is not just about income—it’s about volatility and risk exposure. High earners may have more assets, but they are also more affected by investment fluctuations, market uncertainty, and economic downturns.

Demographically, financial concern is also shaped by political and social factors:

Gen Z (51%) and Millennials (52%) are the most financially anxious generations.

Women (51%) are more financially concerned than men (45%).

Non-white respondents (53%) report greater financial anxiety than white respondents (48%), with Native respondents leading at 60%.

These disparities highlight systemic financial pressures that vary across age, gender, and race, reinforcing the reality that economic challenges are not equally distributed.

How Inflation Is Reshaping Financial Planning

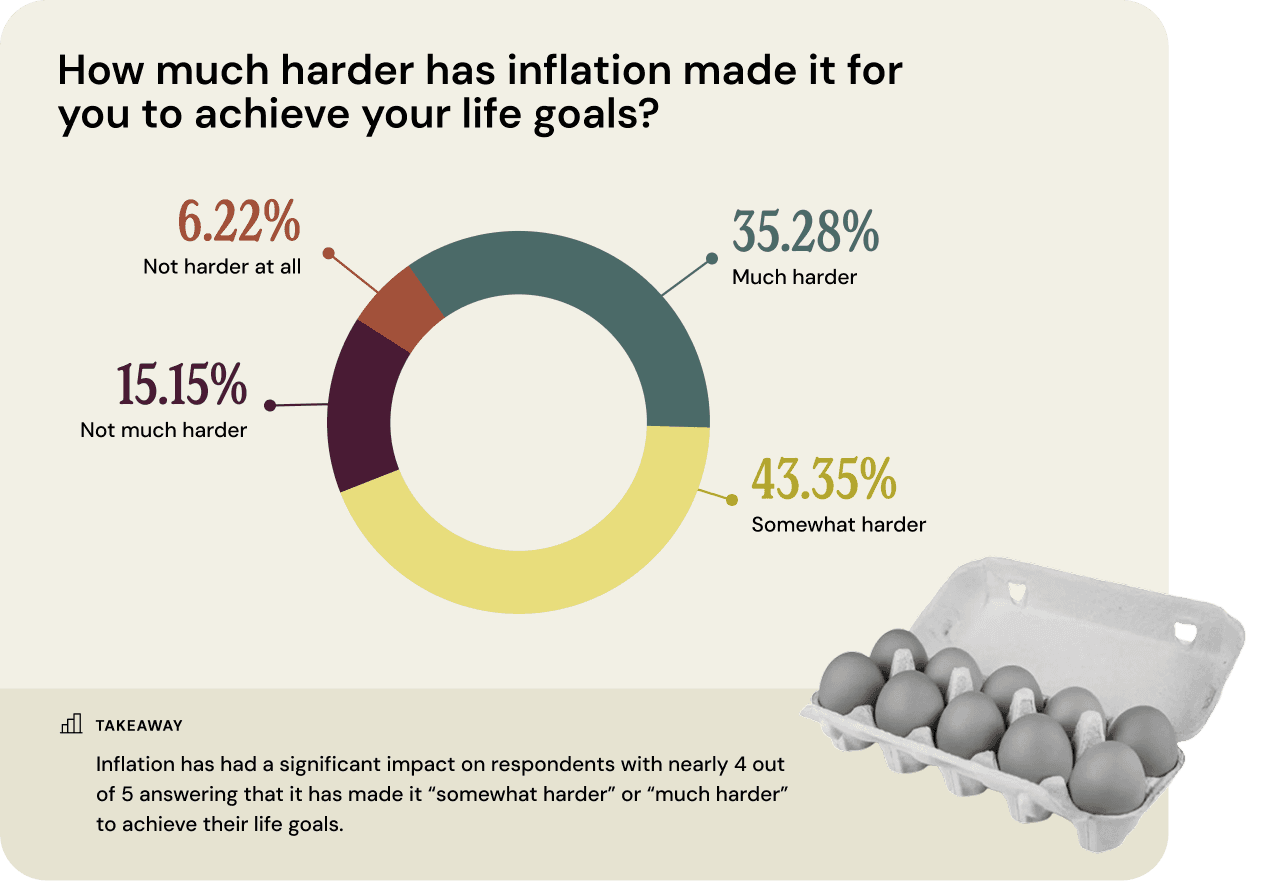

Inflation has fundamentally altered how Americans think about financial security, with nearly four in five people (78%) saying it has made their goals harder to achieve.

43% say inflation has made life goals “somewhat harder.”

35% say inflation has made life goals “much harder.”

Only 6% say inflation has had no impact on their financial trajectory.

While inflation is a universal burden, its impact varies widely by income level:

Gen X (40%) is the most likely generation to say inflation has made their goals “much harder.”

Surprisingly, both low-income earners (<$25K) and high-income earners (>$1M) are the most likely to say inflation has made their goals “much harder” (both at 44%).

By contrast, those earning $250K–$499K are the least likely to feel impacted by inflation—only 17% say it has made their goals “much harder.”

So why are the lowest and highest earners experiencing the greatest financial strain? Lower-income Americans tend to struggle with basic cost-of-living increases (rent, groceries, gas). Higher-income Americans, on the other hand, may face significant market volatility (investments, property values, and business costs). The middle-income bracket ($250K–$499K) appears most insulated, with stable salaries and moderate cost-of-living flexibility.

This two-pronged financial pressure means that while estate planning has traditionally focused on wealth-building, modern estate planning must also account for financial risk management.

Securing the Future in an Unstable Economy

The cost-of-living crisis is not just an economic issue—it is fundamentally reshaping how Americans think about their financial future, long-term goals, and legacy.

Nearly half (49%) of Americans feel more financially anxious than they did last year.

78% say inflation has made it harder to achieve their life goals.

Concern is not exclusive to lower-income individuals—even those earning over $500K express record-high financial anxiety.

Financial security is no longer just about how much money you have—it’s about how well you can protect it. Estate planning in today’s world must adapt to the realities of inflation, economic uncertainty, and financial volatility to ensure that Americans, regardless of income, can secure their future and provide for those they love.

These insights were unveiled in the groundbreaking 2025 Trust & Will Estate Planning Report—the largest estate planning survey ever conducted. Click here to view the full report.

Trust & Will is an online service providing legal forms and information. We are not a law firm and we do not provide legal advice.

Last updated: March 20, 2026

- Share