Top 10 Common Misconceptions Clients Have About Estate Planning

What are some of the most common misconceptions that people have about estate planning? Financial advisor Samuel Deane breaks it down.

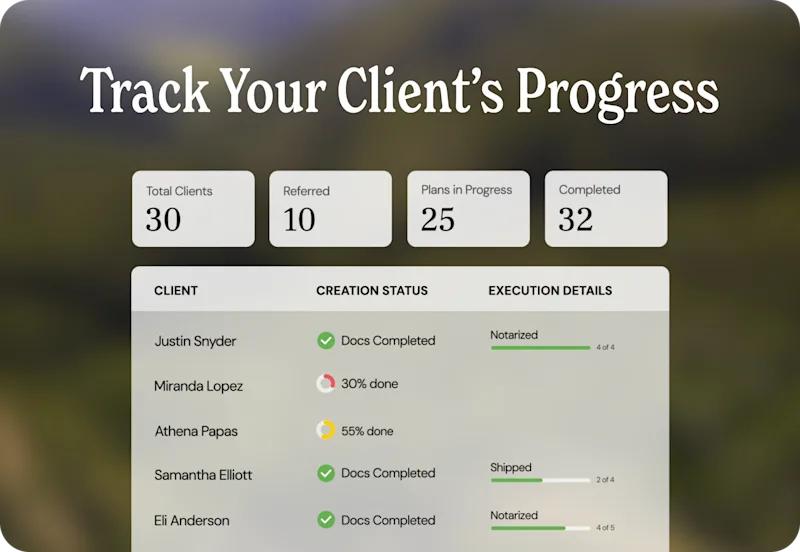

Click here to sign up for your free advisor account and learn how Trust & Will can elevate your advisory services!

By Samuel Deane

Founder, Deane Wealth Management

Let’s debunk some common misconceptions your clients have about estate planning

Estate planning is an essential aspect of financial planning, and it's a great topic to discuss with clients and their families. What I find interesting is that with every "intro to estate planning" meeting we have, some misconceptions always find their way into the conversation. It never fails. Leading with education has served my clients well over the years, and I have a feeling it will do the same for your clients. So, let's debunk 10 common estate planning misconceptions to arm our clients with the education we wish we had in school.

1. I don't have enough assets

Many people believe estate planning is only for the rich. And it's not their fault. Let's think about how the media plays a role. In pop culture, estate planning is often associated with high-net-worth individuals and is depicted in movies, TV shows, and books as something only millionaires and billionaires need to worry about. It's easy to see how this portrayal can mislead people into thinking it's irrelevant to the average person. More education is also needed, as many people may need help understanding what estate planning entails. The term alone has this grandiose tone that can lead people to believe it's beyond their financial reach. Most people don't realize an estate simply refers to their assets and belongings, regardless of their value. In reality, anyone with assets, including a house, savings, or investments, can benefit from estate planning.

2. I'm too young to need an estate plan

My practice works primarily with Millennials, so I hear this one about once a month. From my experience, younger adults often have pressing financial concerns like student loans, starting a family, buying a house, or building a career. Oddly, although most of those life events should trigger creating an estate plan, it becomes less urgent compared to those immediate priorities. The truth is that estate planning is essential for everyone, regardless of age. Even if they don't have many assets or have a negative net worth, clients still need to have a plan in place in the event of their untimely death or incapacity. Financial planners and estate planning professionals need to educate young clients about the advantages of starting early. They should emphasize that estate planning is not just about wealth transfer but also about ensuring their wishes are carried out, protecting their loved ones, and making difficult decisions easier for family members. Starting early can provide peace of mind and financial security, even for young individuals.

3. My digital assets will automatically be passed on to my loved ones

In today's world, everyone has a digital footprint. Digital assets have become increasingly important in our lives and should be considered in your client's estate plan. Assets can include anything from social media accounts to cryptocurrency and digital files. However, one of the biggest challenges with digital assets is that they can be difficult to access if you're not the intended user. That's why keeping a schedule of digital assets with seed phrases and sharing it with a trusted family member or friend is important. To that point, when creating their estate plan, clients should consider the following questions about their digital assets:

Who do they want to have access to their digital assets after they die?

What instructions do they have for how their digital assets should be managed? For example, do they want their social media accounts to be deleted or memorialized? Do they want their cryptocurrency to be liquidated and distributed to your heirs?

How will their loved ones be able to access their digital assets after they die?

4. DIY estate planning is sufficient

True story: I once had a client who mentioned creating a Will using an online template he found on Google. DIY estate planning can be an option for some individuals, but clients need to understand the pros and cons. For instance, it is typically less expensive than hiring an attorney, and there are online tools to make it relatively easy to create basic estate planning documents. However, estate planning is not a one-size-fits-all endeavor and unique circumstances may require specialized documents or legal expertise. What works for one person may not be appropriate for another. Additionally, each state has its own laws and requirements for estate planning documents, and templates may not be up-to-date or compliant. I can go on about the cons of taking a DIY approach, but I'm sure you get the point.

5. I don't need a Will because I'm single with no kids

My favorite thing to say to clients is this: "Everyone has an estate plan. It's a question of whether your state court will determine your estate plan or will you." Even if your clients are unmarried and don't want to have children, they still need a will. Without one, their assets will be distributed according to their state law, which may not be what they want.

6. Estate planning is only about what happens after I die

I'm proud to work with clients from many cultures, and I've noticed that discussions about end-of-life topics, including death and inheritance, can be considered taboo or uncomfortable. As a result, people naturally limit their understanding of estate planning to post-death scenarios. In reality, there are plenty of aspects to estate planning that include provisions for one's well-being and decision-making throughout their lifetime, especially in cases of incapacity. By having a plan in place, clients can designate someone they trust to make financial and medical decisions on their behalf. This includes decisions about healthcare, finances, and guardianship for minor children. As financial advisors, we need to promote a holistic understanding of estate planning so our clients can appreciate its relevance to their lives, not just its end.

7. My family will sort everything out

It's not uncommon for clients to assume their family members inherently understand their desires and preferences, primarily if they've engaged in informal conversations about assets, inheritances, and intentions regarding their estate. A strong sense of trust in close-knit families can also lead clients to believe that their loved ones will naturally prioritize their wishes and act in their best interests. I'm grateful not to have any real-world experiences, but these arrangements can go south very quickly. In other words, relying on family to figure things out can lead to disputes and complications. Proper estate planning can help prevent these conflicts and provide clear guidance for your clients and their loved ones.

8. A Will is all I need

At the root, this comes down to education or lack thereof. While a will is an integral part of estate planning, it's not the only document clients need. Trusts, powers of attorney, and healthcare directives can also ensure your client's wishes are fulfilled. For instance, if a client passes away without their home in a Trust, the property will only be distributed to their beneficiaries after completing the probate process. Even then, the decision can be contested by disgruntled family members. On the other hand, using a Trust, the home can be distributed directly to beneficiaries without an extensive and expensive probate process.

9. Estate planning is expensive

While it's true that estate planning can be complex, it doesn't have to be expensive. In general, the perception of estate planning being expensive has been influenced by several factors, like fear of hidden costs, working with attorneys, and lack of fee transparency by professionals in service industries. But it's much more affordable and accessible for clients with simple estates than one might assume. Let's look at Trust & Will as an example. Leveraging the platform, our RIA has been able to help more than 95% of new clients create an estate plan within the first 12 months of working together. This is primarily because of the convenience and affordability that Trust & Will provides.

10. It's a one-time task

Clients with relatively simple financial situations may assume that their estate plan is straightforward and doesn't require updates. Others may believe that their life circumstances and financial situation will remain stable once they have created an estate plan. Contrary to popular belief, estate planning is not a set-it-and-forget-it task. It should be reviewed and updated regularly to account for changes in your clients' lives, such as marriage, divorce, birth, death in the family, or changes in their financial situation.

As financial advisors, we know that life is dynamic, and clients' circumstances can change over time. By addressing misconceptions and promoting the need for ongoing planning, financial planners help clients adapt their estate plans to new developments in their lives. At the bare minimum, educating clients about these misconceptions and helping them create a comprehensive estate plan that aligns with their goals is essential to any financial planner's role.

New to Trust & Will and want to see how it works? Book a demo to discover how Trust & Will can elevate your advisory services and better support your clients' estate planning needs.

Trust & Will is an online service providing legal forms and information. We are not a law firm and we do not provide legal advice.

Last updated: February 16, 2026

- Share