What is a Trust & Why do You Need One?

Learn everything you need to know about Trusts including types of trusts, who needs one and how to get a trust in this comprehensive guide by Trust & Will!

By Craig Parker

Assistant General Counsel, Trust & Will

Trusts Explained: A Tool for Families, Property, and Privacy

When someone hears the word "Trust," there are usually certain images that come to mind. Things like "wealthy trust fund babies" and elderly individuals with high net worths, to name a few. The truth is, however, more people benefit from having a Trust than you probably think.

If you're looking for the best, most comprehensive way to protect your family after you're gone (and you're a homeowner with at least $160,000 of assets) a Trust will likely be the ideal Estate Plan option for you. Creating your Will is another protective measure you can take to safeguard your assets and loved ones if you're not quite ready or don't yet qualify for a Trust. And don't worry — you can always add a Trust to your Estate Plan as your life evolves.

In short, a Trust is a fiduciary agreement that’s part of an Estate Plan. Traditionally, Trusts are used to hold assets for one or more Beneficiaries, and they may offer significant estate tax and other protective benefits. If you're considering setting up a Trust — or any type of Estate Plan for that matter — our guide is the right place to start.

Not sure which type of Estate Plan will best meet your needs? Take our simple quiz to find the perfect fit. If you'd still like to learn more about Trust, keep reading to discover:

What is a Trust?

A Trust is a legal fiduciary arrangement that allows you to set up your assets to be held and managed by a third party. This party is known as a Trustee, and the person or firm you appoint to this role will be responsible for ensuring that your estate is handled in the manner you’ve outlined.

Despite what many people think, Trusts can be beneficial for all sized-estates, not just very large ones. There is a common misconception that an Estate Planning Trust is only suitable for the extremely wealthy. But the reality is, there are many benefits to a Trust, including:

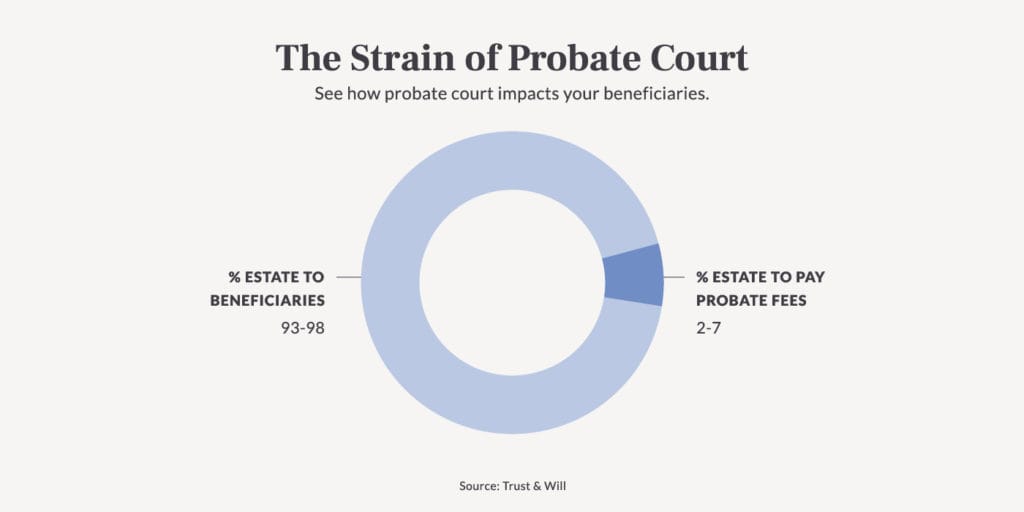

Avoiding probate court so Beneficiaries can receive assets sooner

Privacy

Protection

Reduced or eliminated estate and gift taxes

The ability to better-control future wealth by establishing conditions for asset-distribution

This misconception has real consequences: Trust & Will's 2026 Estate Planning Report found that only 1 in 10 Americans currently has a trust — a stark gap given how many households could benefit from one.

There are multiple types of Trusts, and it’s important to really assess your needs and goals before you decide on which type you’ll create. We’ll discuss in more detail the types of Trusts below.

What is the Purpose of a Trust?

There are several purposes of an Estate Planning Trust, but one of the more common reasons people choose to use them is to better-ensure their assets are handled exactly as they wish, from the moment the Trust goes into effect, until long after passing. They can also be used as a means to manage tax consequences on an estate. And, they’re a way to potentially protect your wealth while still qualifying for Medicaid in your later years.

Trusts are often used in cases where someone wants or needs to set up financial care for young children or long-term planning and care for dependents with disabilities.

Who Should Have a Trust?

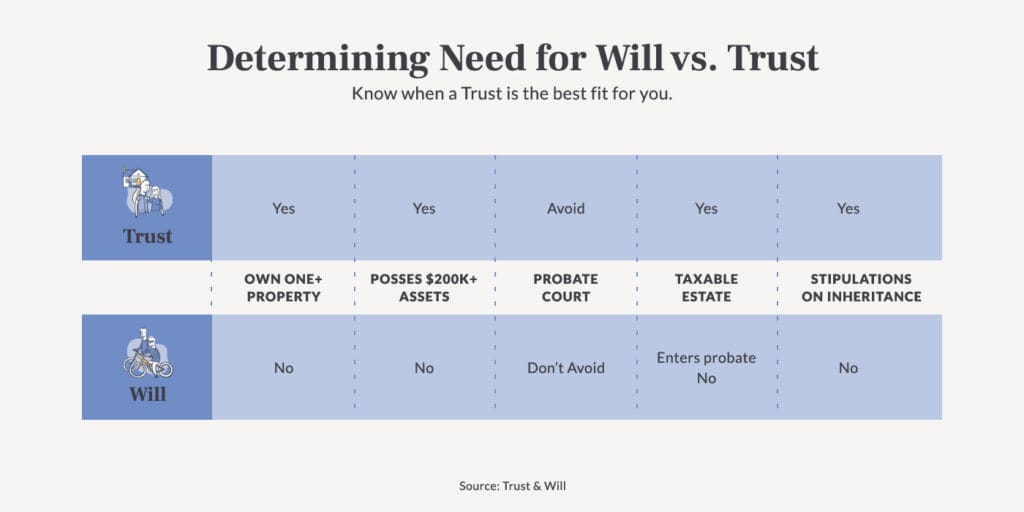

Trusts aren’t necessarily the best solution for everyone. There are several reasons a Trust might make sense, but that doesn’t mean absolutely everybody needs one. A Trust may be beneficial for those in specific situations, such as:

You own a home or other property, particularly if it’s out of state

You have $200k+ in assets

You wish to keep your assets private

You are hoping to simplify the probate process for your loved ones after you pass

You have a taxable estate – keep in mind the qualifying value that deems an estate “taxable” will differ from state to state

You want to set up stipulations on inheritances – for example, awarding a dollar amount for certain life events such as graduating college, getting married, etc.

Ready to create your Trust?

Setting up and funding a trust doesn't have to be complicated. Trust & Will guides you through every step with our online platform. From creating your trust document to ensuring it's properly funded. Get started in minutes and have peace of mind that your estate is protected.

Types of Trusts

As noted, there are several types of Trusts, each with its own nuance and purpose. Before establishing a Trust, be sure to have a clear idea of your goals so you can use the type of Trust best-suited to accomplish them.

Living Trust

A Living Trust is created during your lifetime and it designates a trustee who will manage assets for your Beneficiary or Beneficiaries after your passing.

Revocable Living Trusts

A Revocable Living Trust is created during your lifetime and can be altered or revoked while you’re alive. It is used to avoid probate, but while you’re alive, it's not an ironclad technique for asset protection. Any assets in your Revocable Living Trust will still be available to creditors during your lifetime, although it will be more difficult for them to gain access.

Irrevocable Trusts

An Irrevocable Trust means you cannot change or alter anything in the Trust once it’s established. You have legally removed any rights to ownership to anything you put in the Trust. In some cases, an Irrevocable Trust may be used as a way to protect assets from creditors or bypass estate tax, as you will have effectively removed yourself as owner for any of the assets inside the Trust. Irrevocable Trusts can be beneficial for those in professions that are vulnerable to lawsuits, such as attorneys or doctors.

Joint Trusts

A Joint Trust is a Trust established for two people, like husband and wife. While both parties are alive, they maintain total control over any and all assets that are in the Trust. They can change the Trust at any time, and after one partner passes, the surviving partner becomes Trustee.

Testamentary Trusts

A Testamentary Trust is a Trust that’s created within a Will, and it only goes into effect upon your passing. Also known as a “Trust Under Will” or a “Will Trust,” the Last Will and Testament instructs how the actual Trust should be established. Because the Trust isn’t truly created until after you pass, it’s not considered a Living Trust. It’s important to note that this option results in the Will going through probate. And, there’s also diminished privacy protection that some Trusts offer, as the Trust terms are described in the Will.

Revocable vs Irrevocable Trust

A Revocable Trust can be changed at any point during your life as long as you’re of sound mind. By contrast, an Irrevocable Trust is the exact opposite. It cannot be changed, and furthermore, you no longer own assets once you place them into an Irrevocable Trust. It may seem like an Irrevocable Trust is never a good idea, but under certain circumstances, it actually can be beneficial. For example, if you are at risk for lawsuits due to your profession, an Irrevocable Trust can protect and preserve your assets from judgments, creditors and liens.

How to Set up a Trust

Trust & Will makes setting up a trust easy. The following sections provide an overview of what you need to know, including what you may want to add to your trust, how to name it, and very importantly, how to fund your trust. (This is the process of making sure the assets you want to put in the trust are properly titled to it by transferring ownership to the trust.)

Our resident legal expert explains how to set up a trust in this guide here.

What to Add to a Trust

There are certain assets that are appropriate to fund your Trust. To accomplish this part of the process, you will retitle assets with the Trust as the owner. The types of assets a Trust can hold include:

Home(s) or other real estate

Tangible property like jewelry, antiques, collectibles, vehicles, etc.

Retirement accounts – naming the Trust as beneficiary

Brokerage accounts and non-retirement investments can be retitled in your Trust’s name

Cash accounts, including savings and checking accounts, money markets and CDs – note that transferring CDs needs to be handled carefully so you’re not penalized for an early withdrawal of funds during the retitling process

Large assets

Business interests

Stocks or bonds that are held in certificate form

Non-qualified annuities

How to Name a Trust

Choosing a name for your Trust is the easy, but important part. Most people name a Trust something logical and representative of their family. This makes sense, as it makes it easy to remember, so when you’re renaming all the assets the Trust will hold, it’s a logical process. Your family name (and possibly the date the Trust is established), along with the words “Family Trust” at the end, is a simple formula that’s commonly used. Using this format or something similar to it leaves very little room for any misinterpretation as to what the Trust document is. Date can be used as an organizational tool, or it can be left off entirely.

How to Fund a Trust

Once you have created and named your Trust, the next step is funding your Trust. Funding a Trust simply means you are moving assets into the Trust, making the Trust the new owner. Keep in mind, your Trust is a vehicle designed to hold and protect your assets. Until you put said assets into it, it really holds no value or has any purpose. There is a pretty straightforward process to move appropriate assets into a Trust. Much of it just involves renaming an asset to be Trust-owned.

Individual assets can have slightly different processes, so be sure to check each one. For example, to put real estate into your Trust, you will need the deed, and if you have a mortgage on the property, it’s possible, but not likely, that you might need permission from your lender. If you’re transferring bank accounts into your Trust, you should check with your bank for the specifics on paperwork.

Other Common Questions about Trusts

Differences Between a Will and a Trust

The biggest difference between a Trust and a Will is that a Trust goes into effect as soon as it’s created, whereas a Will only becomes effective after you pass. There are also tax implications specific to each, and Trusts can remain private and avoid probate, whereas the process of passing property per the terms of a Will will be both public and go through probate.

What is a Trust Fund?

A Trust Fund is an effective tool that’s often used in Estate Planning wherein a Grantor (you) sets up a plan that will ensure financial stability and security of a Beneficiary, often a child or grandchild. A Trust Fund can hold investments, cash, real estate and other assets to be distributed in the future.

What is a Trustee?

A Trustee is the person you name to be responsible for your Trust assets. In essence, the Trustee is the legal owner of everything in the Trust. He or she is charged with administering (distributing) assets or property for the benefit of your named Beneficiaries, as defined in the Trust. The Trustee is also responsible for handling the Trust’s tax filings.

Can a Trustee Be Removed From a Trust?

A Trustee can be removed from a Trust under certain conditions. For example, if they have not lived up to the responsibilities outlined in the Trust, if they no longer wish to perform or are incapable of the duties, or as specified in the Trust. You can outline ways to remove a Trustee, such as stating all Beneficiaries must agree they want to change who is appointed.

Can a Trustee Use Money From the Trust ?

Trustees can only use the money or assets in the Trust to provide for Beneficiaries or to accomplish other Trust-related responsibilities. A Trustee cannot use Trust money for personal use or benefit.

What Is An A-B Trust?

An A-B Trust is used to minimize estate taxes. Also known as a Credit Shelter Trust or a Bypass Trust, it’s a Joint Trust that a husband and wife create together. A-B Trusts will divide into two separate Trusts once the first partner passes. At that time, Trust A becomes what’s referred to as the Survivor’s Trust, and Trust B is the Decedent’s Trust. This type of Trust can be tax beneficial for those with very large estates ($11.58m or larger) to avoid heavy estate taxes for Beneficiaries. A-B Trusts allow a surviving spouse to use and benefit from Trust assets, but prevents them from changing any distribution plans. They’re often used in circumstances with blended families or remarriages so that surviving spouses can not leave assets to only their own children.

Can I Put My Vehicles In My Trust?

You can transfer cars to your Trust, but one concern is insurance. Some insurance companies don't have a great system for handling Trusts. That could mean you would need to name the Trust, Trustees and/or Beneficiaries as "Additional Insureds," or get special riders from your insurance carrier, which can be a hassle. Because of this, some people choose not to put their personal vehicles in their Trust. Instead, they rely on the Pour-Over Will to say any vehicles go into their Trust at death. Letting assets pass under the Will might mean the Will has to go through probate, but the values of the cars are usually low enough that it's just a simplified probate process. Note that this is true for daily driver cars, but collector or valuable cars might be different.

Setting up your Trust is beneficial on many levels. It’s one of several layers of your Estate Plan, and it’s yet another safeguard against things happening against your wishes once you no longer have a say. Providing security, passing on your hard-earned personal wealth and assets, and setting up a tax-beneficial estate is one of the best gifts you can leave your heirs. Knowing and trusting that they will be taken care of, even when you’re not there to do it, is priceless.

Still wondering if a Trust-Based Estate Plan is right for you? Take our simple quiz to help you make that decision!

Related Topics

Last updated: June 4, 2026

- Share